Oral GLP-1 and Beyond: The Emerging Structural Disruption in Diet Drugs Driven by Formulation Innovation

Oral glucagon-like peptide-1 (GLP-1) receptor agonists, exemplified by the semaglutide pill, represent a quiet but profound inflection in obesity and diabetes pharmacotherapy. This development could reshape patient access, expand markets, and necessitate regulatory and industrial realignments over the next decade. The evolving formulation technologies underpinning injectable-to-oral transitions signal more than incremental drug delivery improvements—they may catalyse systemic change in how metabolic diseases are managed globally.

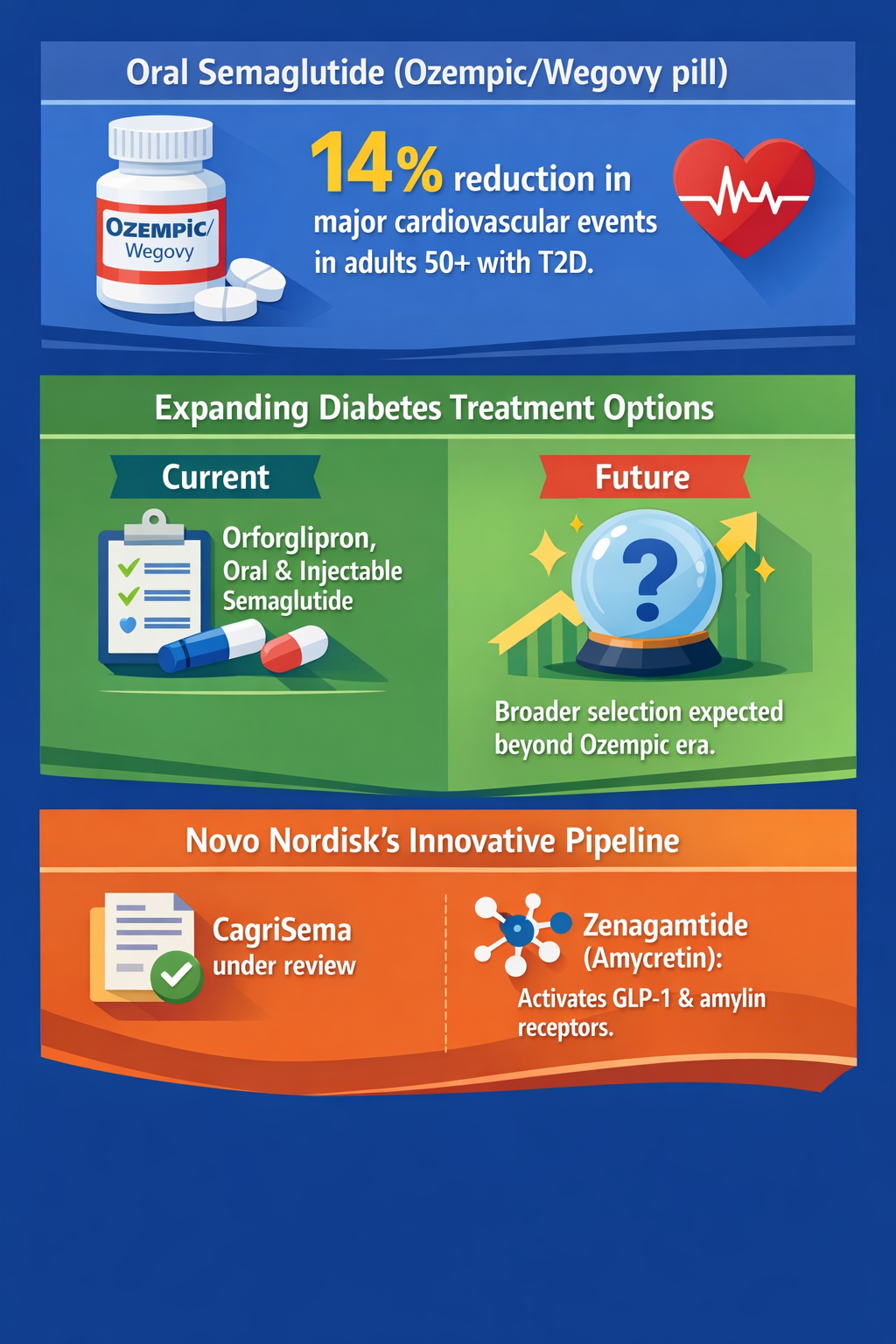

The oral semaglutide innovation, showcased by Novo Nordisk’s Ozempic and Wegovy pills, is seeding a wider pipeline of oral and injectable candidates, pointing toward a future with broader, user-specific treatment modalities for obesity and type 2 diabetes (T2D). This offers an underappreciated lever for scaling access and modifying risk stratification, with ripple effects for payers and manufacturing ecosystems.

Signal Identification

This development qualifies as an emerging inflection indicator due to its potential to alter existing pharmaceutical industrial paradigms by combining formulation technology advances with metabolic disease treatment. The signal lies not only in the oral form itself, but in the broader diversification of administration routes and patient-segment-specific formulations now entering late-stage clinical pipelines (Life Science Daily 14/02/2026). Its plausibility is high given recent approvals and clinical evidence supporting cardiovascular event risk reduction from oral semaglutide (Pharmacy Times 12/01/2026). The time horizon spans 5 to 10 years, with exposures concentrated in pharmaceuticals, healthcare delivery, regulatory affairs, and supply chain logistics.

What Is Changing

The transformative development is the move from injectable GLP-1 receptor agonists toward oral formulations that retain efficacy while expanding patient acceptability and adherence. Semaglutide’s oral entry into markets such as the UK following Medicines and Healthcare products Regulatory Agency (MHRA) approval signals a strategic pivot toward less invasive treatments (Food Ingredients First 22/03/2026). This trend is undergirded by a surge in formulation development capabilities, notably in fill-finish services optimized for peptides (including GLP-1), which is expected to grow rapidly and underpin production scale-up (Precedence Research 05/01/2026).

Concurrent expansion of the obesity drug pipeline, including novel oral and injectable options beyond semaglutide and orforglipron, points to a future with differentiated treatments targeting a continuum of metabolic disease stages (Life Science Daily 14/02/2026). This signals a shift from a “one-size-fits-most” model to more granular product tailoring. Additionally, anticipated policy shifts like the proposed Medicare GLP-1 Bridge could redefine affordability thresholds and broaden market access in the US, which is a critical dimension considering current high drug prices (Duncan Market Insights 18/02/2026).

The recurring theme is that innovations in oral peptide delivery are enabling wider, earlier, and potentially preventive use of these medicines, which historically were limited by injection burdens and thus adherence challenges. This decentralizes and democratizes access and could recalibrate patient risk profiles and payer strategies.

Disruption Pathway

The oral GLP-1 development can plausibly evolve into structural change by first accelerating patient uptake due to ease of administration and broader clinical applicability, which exerts pressure on current healthcare delivery and reimbursement models reliant on injectable therapies. Should coverage expansions like the Medicare GLP-1 Bridge come to fruition with issuer-friendly terms, payer willingness to finance these drugs may increase markedly, broadening demand and necessitating shifts in formulary design.

Pharmaceutical manufacturers and contract development and manufacturing organizations (CDMOs) will face stresses requiring scale-up of oral peptide formulation capabilities. These could lead to industry consolidation around specialized fill-finish and formulation technologies, raising barriers to entry for innovators without such assets.

Regulatory frameworks may adapt to incorporate stage-specific formulations and combination therapies targeting cardiometabolic risk profiles, necessitating updated clinical evaluation criteria and post-market surveillance models. Feedback loops may emerge where increased use reduces incidence of downstream costs from cardiovascular events, reinforcing payer incentives to embrace these treatments sooner in disease progression.

However, unintended consequences may arise if broad access without tailored patient stratification leads to inappropriate use or liability exposures. This dynamic could trigger more stringent regulatory oversight or risk-sharing agreements. Strategic positioning will therefore shift as incumbent GLP-1 manufacturers diversify portfolios into oral formulations, integrate vertically with CDMOs, and expand into adjacent cardiometabolic markets.

Why This Matters

This signal bears direct implications for capital allocation as pharma companies, manufacturers, and CDMOs recalibrate investment toward oral peptide technologies. Payers and regulators will confront emerging cost-benefit paradigms driven by efficacy data showing outcomes beyond glycemic control, including cardiovascular risk reduction (Pharmacy Times 12/01/2026).

Competitive positioning may tilt toward integrated firms capable of end-to-end development and scalable, flexible manufacturing of oral and injectable formulations, introducing new supply chain dynamics. Governance systems will need to evolve in terms of post-market monitoring to capture real-world evidence in diverse patient populations now enabled by oral administration ease. Liability and reimbursement models will be stressed by uncertainties in long-term safety and usage patterns in expanded populations.

Implications

This development may reshape the industrial landscape by elevating formulation innovation from a supporting function to a strategic core. It could catalyse a structural shift whereby metabolic disease treatment adopts a more preventive, multi-modal, and patient-centric model. Oral GLP-1 formulations might displace many injectable options, reducing healthcare delivery burdens and expanding global markets.

However, these changes should not be conflated with transient hype around novel obesity drugs alone; rather, this is a fundamental shift in drug delivery and disease management paradigms. Competing interpretations might argue that reimbursement challenges or patient adherence variability could limit scale, but current policy initiatives and clinical data make these outcomes increasingly unlikely.

Early Indicators to Monitor

- New patent filings on oral peptide formulation technologies and fill-finish processes

- Regulatory submissions and approvals of additional oral GLP-1 receptor agonists and combination products

- Policy drafts regarding expanded Medicare or national health coverage schemes for obesity and T2D medications

- Venture funding concentration in oral peptide CDMOs and related manufacturing innovation startups

- Capital expenditure announcements by pharmaceutical companies into formulation and delivery technology infrastructure

Disconfirming Signals

- Regulatory setbacks or safety concerns specific to oral GLP-1 formulations limiting approvals or market withdrawals

- Policy reversals or payer refusal to expand obesity and diabetes drug coverage under public insurance schemes

- Technological failures to scale oral peptide manufacturing efficiently or economically

- Significant patient adherence or real-world effectiveness shortfalls compared to injectables

Strategic Questions

- How should capital allocation shift to prioritize oral peptide formulation capabilities within pharmaceutical portfolios and CDMOs?

- What regulatory frameworks and surveillance mechanisms are needed to govern the expanding diversity of GLP-1 administration modes and patient segments?

Keywords

oral semaglutide; GLP-1 receptor agonist; formulation innovation; peptide therapeutics; fill-finish services; metabolic disease; Medicare coverage; pharmaceutical supply chain

Bibliography

- Oral semaglutide (Ozempic pill, Wegovy pill; Novo Nordisk) reduced the risk of major adverse cardiovascular events by 14% in adults with T2D aged 50 or older who had elevated cardiovascular risk. Pharmacy Times. Published 12/01/2026.

- Only orforglipron and the oral and injectable semaglutide products are approved, but the depth of the phase 3 pipeline suggests the choice facing patients in the next few years will be far wider than the one that defined the Ozempic era. Life Science Daily. Published 14/02/2026.

- The Medicare GLP-1 Bridge could make a medication that felt impossible suddenly affordable, or it could come with caveats that matter for your budget. Duncan Market Insights. Published 18/02/2026.

- The move to an oral semaglutide pill could expand the GLP-1 user base and increase demand for use-stage-specific formulations in the UK. Food Ingredients First. Published 22/03/2026.

- The formulation development & fill-finish services segment is expected to grow at the fastest CAGR in the coming years, owing to the increasing need for injectable peptide therapies, such as GLP-1 receptor agonists for diabetes and obesity. Precedence Research. Published 05/01/2026.