The Quiet Rise of Petrostates as Urban Innovation Hubs: A Weak Signal Reshaping Megacity Futures

Urbanization and megacity evolution are conventionally viewed through demographic growth, infrastructure scaling, and digital transformation lenses. Beneath these well-trodden narratives, an under-recognized signal exists: the catalytic role of national oil and petrochemical giants in shaping urban innovation ecosystems—particularly in emerging regions. This development may transform capital flows, industrial clustering, and regulatory paradigms over the next two decades.

This insight paper highlights how petrochemical product innovation, deployed by firms such as Saudi Aramco, is seeding new city-scale industrial metabolisms in the Middle East, Africa, and parts of Asia. This dynamic challenges prevailing assumptions about urbanization being primarily driven by population and digital economies, revealing a structural pivot where energy-materials corporates drive urban-industrial integration. The paper assesses pathways for this weak signal to catalyse systemic changes in urban governance, infrastructure planning, and cross-sector capital reallocation.

Signal Identification

This development qualifies as a weak signal because it is currently overshadowed by dominant urbanization themes—digital skills gaps, demographic pressures, and traditional FDI flows—but has high plausibility to scale into fundamental changes in industrial and urban systems over a 10–20 year horizon. The signal is medium to high in plausibility due to accelerating investments in petrotechnologies by regional champions like Aramco and emergent policy frameworks in resource-rich nations supporting integration of petrochemical innovation in urban development (Farmonaut 25/05/2026; Cushman & Wakefield 14/04/2026). Exposed sectors include urban infrastructure, real estate development, energy materials manufacturing, and regulatory governance frameworks.

What Is Changing

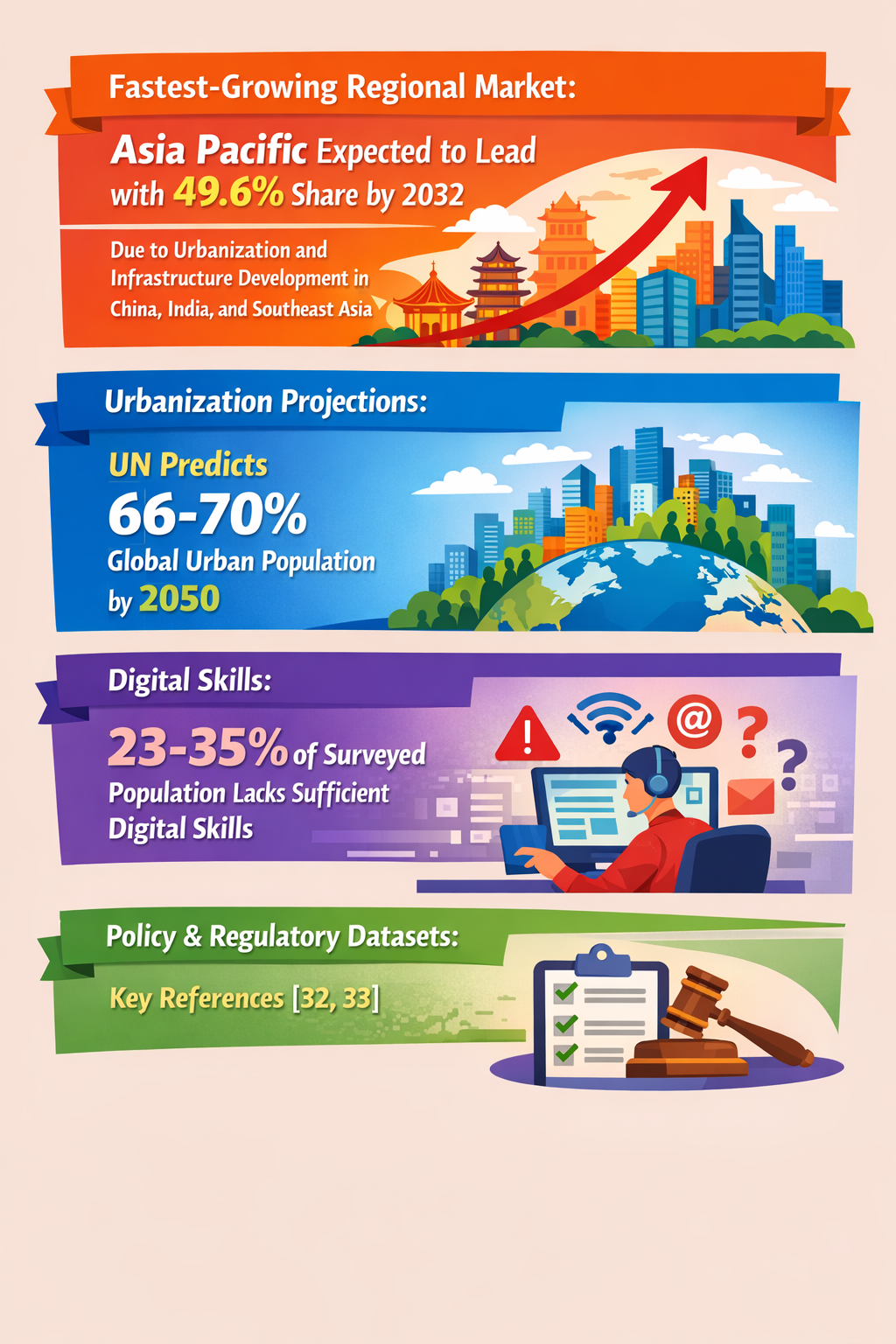

Global urban growth projections consistently estimate that by 2050, 66–70% of populations in Asia, Africa, and the Middle East will reside in cities (PMC 12/06/2025). Simultaneously, there is an increasing recognition that digital skill shortages—estimated at 23–35% in affected regions—could constrain purely tech-driven urban economies. Against this backdrop, petrochemical innovation is emerging as an overlooked structural driver supporting urban industrial diversification and capacity building.

Saudi Aramco’s investments into proprietary materials and chemicals (CPP, CPC product lines) are facilitating new industrial clusters aligned with urban expansion plans in the Middle East and parts of Asia. This innovation pipeline includes advanced polymers, composites, and sustainable petrochemicals designed for infrastructure applications, renewable energy systems, and high-value manufacturing (Farmonaut 25/05/2026).

Furthermore, Southeast Asia’s urban real estate markets are seeing structural uplift as supply chain diversification and sustained foreign direct investment (FDI) intersect with expanding industrial innovation in chemicals and materials, which underpin building technologies and urban utilities (Cushman & Wakefield 14/04/2026). This nexus strengthens urban ecosystems beyond transit and digitization, embedding energy materials firms as anchors in city industrial metabolisms.

Concurrently, rising urbanization paired with wage growth and nutrition outreach programs indicate an evolving socio-economic profile in Asia-Pacific megacities, which may further catalyse demand for advanced materials related to healthcare infrastructure and fortified food packaging, linking petrochemical innovations directly to urban well-being frameworks (Reanin 02/04/2026).

Collectively, these insights reveal a substantive shift: urbanization is gradually converging not just with digital economies and demographic momentum, but also with petrochemical innovation rooted in national energy champions’ strategies. This is a catalytic industrial-urban hybridization scarcely recognized in current foresight discourse.

Disruption Pathway

Petrochemical product innovation feeding urban growth can escalate through several interlinked mechanisms. Firstly, continuous R&D advances and process optimizations by firms like Aramco could accelerate the development of locally adapted construction materials, energy storage media, and sustainable chemical inputs tailored for urban infrastructure, improving cost and performance metrics relevant to growing megacities.

With these advances, petrochemical hubs embedded within urban areas apply pressure on traditional supply chains that rely more heavily on imported, generic materials. This would drive initial stresses on procurement standards, regulatory certifications, and logistics, stimulating adaptation among urban planners and construction industries.

As these materials innovation ecosystems mature, cross-sector industrial clustering around petrochemical anchors may become a structural feature of megacity development. This clustering would catalyse ecosystem-wide productivity gains, enabling alternative pathways for FDI flows—from passive capital into more active industrial partnerships with energy-materials firms.

Feedback loops may arise whereby urban infrastructure innovations dependent on proprietary material chemistries increase switching costs and investment lock-in into particular petrochemical providers, reshaping competitive dynamics and incentivizing policy environments that favor integrated urban-industrial governance models.

Over time, this may compel a shift in dominant regulatory frameworks across city-states and national governments, integrating energy-material product certification, urban environmental standards, and industrial diversification goals. Capital allocation paradigms may shift accordingly, prioritizing urban projects that leverage local petrochemical innovation over generic infrastructure schemes.

Why This Matters

For capital allocators, recognizing petrochemical innovation as a driver of urbanization could realign investment portfolios towards integrated urban-industrial ventures rather than siloed real estate or digital infrastructure. Such shifts may enhance returns by capturing synergies at the urban materials interface and mitigating supply chain risks from commodity price volatility.

Regulators and policymakers face a need to evolve standards and governance models to address emergent industrial clusters embedded within growing cities, balancing environmental sustainability with industrial competitiveness. Failure to adapt regulatory regimes could lead to stranded urban assets or bottlenecks in critical infrastructure sectors.

Industrial strategists must factor this dynamic into long-term positioning by considering how petrochemical firms could become urban innovation ecosystem keystones, altering competition in construction, utilities, and materials manufacturing sectors. Supply chains linked to petrochemicals may undergo reconfiguration, affecting logistics, procurement, and workforce skills planning in urban contexts.

Liability and risk governance is affected as urban infrastructures increasingly incorporate novel chemical products and energy materials whose long-term performance and environmental impact may not be fully characterized under current frameworks, necessitating new standards for risk assessment and mitigation.

Implications

This weak signal may translate into structural change by reorienting urban growth strategies around resource-product innovation hubs rather than predominantly demographic or digital nodes. Urban-industrial metropolises supported by petrochemical innovation might emerge in resource-rich regions earlier than in others, creating differentiated competitive landscapes.

While not a substitute for digital skills or demographic drivers, petrochemical integration into urbanization could become a principal factor amplifying the scale and complexity of megacity infrastructure investments. It is unlikely to manifest as isolated petrochemical booms but rather as embedded industrial-urban hybrids with system-wide effects.

Competing interpretations might characterize this as incremental supply chain realignment rather than a paradigm shift; however, the broad industrial, regulatory, and governance implications documented suggest potential for deeper structural transformation.

Early Indicators to Monitor

- Increasing patent filings and R&D disclosures by national energy firms related to urban materials and infrastructure applications.

- Procurement contracts in urban infrastructure explicitly favoring petrochemical innovations in construction materials or utilities.

- Drafting or adoption of regulatory standards addressing petrochemical-based urban building products and environmental controls.

- Clusters of venture funding or FDI directed towards petrochemical innovation parks integrated with urban development zones.

- Capital reallocation from traditional infrastructure projects to integrated urban-industrial development in Middle East, Africa, and Asia regions.

Disconfirming Signals

- Stagnation or reprioritization of petrochemical R&D spending away from urban materials innovation.

- Regulatory rollbacks or moratoria disallowing use of new petrochemical products within urban development programs.

- Major disruptions in oil and gas supply chains curtailing feedstock availability for advanced materials production.

- Successful digital skill development and demographic transitions outpacing the utility of petrochemical-driven urban industrialization.

- Persistent geopolitical instability preventing integration of petrochemical innovation hubs with urban planning authorities.

Strategic Questions

- How can capital allocation strategies incorporate petrochemical innovation as a systemic driver of urban industrial ecosystems?

- What regulatory reforms are necessary to support the integration of advanced petrochemical materials into sustainable megacity infrastructure?

Keywords

Urbanization; Megacities; Petrochemical Innovation; Capital Allocation; Industrial Clusters; Regulatory Frameworks; Urban Infrastructure; Supply Chain; Emerging Markets

Bibliography

- The future of urbanization in the Middle East, Africa, and parts of Asia will be deeply shaped by Aramco CPP, Aramco CPC, and CPC Aramco materials and innovations. Farmonaut. Published 25/05/2026.

- Social and demographic datasets comprised UN urbanization projections (66-70% urban population in 2050), digital skills surveys (23-35% insufficient skills), and policy / regulatory datasets like the [32, 33]. PMC. Published 12/06/2025.

- Structural drivers - including supply chain diversification, rising urbanization and sustained foreign direct investment - reinforce Southeast Asia's long-term real estate potential. Cushman & Wakefield. Published 14/04/2026.

- Emerging markets offer high growth potential, especially in Asia-Pacific, where rising urbanization, wage growth and nutrition outreach programs converge. Reanin. Published 02/04/2026.

- Regulatory and policy frameworks shaping urbanization and industrial clusters in resource-rich emerging economies. Cushman & Wakefield. Published 14/04/2026.