Orbital Edge Computing: The Under-Recognized Wildcard Reshaping Connectivity

Orbital edge computing via satellite constellations is an emerging wildcard that could radically transform global connectivity infrastructure and governance. Beyond the familiar hype around 6G and terrestrial IoT, the integration of space-based AI-processing data centers signals a fundamentally new architectural paradigm. This development carries high structural potential over the next 10 to 20 years to disrupt capital allocation, regulatory regimes, and competitive positioning worldwide.

While satellite internet has long been viewed as a niche or stopgap solution, a convergence of accelerating AI services demand, new satellite hardware capabilities, and operator strategies like SpaceX’s planned Starlink mobile push could catalyze a systemic shift. The move to embed compute capability directly in orbit – previously dismissed as futuristic – also raises underappreciated cybersecurity, spectrum governance, and industrial restructuring challenges.

This paper argues that orbitally deployed AI-processing data centers will emerge as a latent inflection point, transforming connectivity from a primarily ground-focused infrastructure to a hybrid terrestrial/space network with profound implications for multiple sectors.

Signal Identification

This development qualifies as an emerging inflection indicator. It is in the early to mid-stage of visibility, with credible technical engineering decisions and commercial plans underway, yet it is largely underestimated in strategic foresight circles that focus on terrestrial 5G/6G evolution.

The time horizon is 10–20 years, reflecting current roadmap milestones such as 6G specifications expected by 2028 and orbital AI centers launched alongside next-gen Starlink satellites as soon as the late 2020s (CNN 24/06/2026). The plausibility band is medium-high given the convergence of private capital interest, proven launch capacity, and technology maturity.

Sectors exposed include telecommunications, cloud computing, cybersecurity, regulatory governance, satellite manufacturing, IoT, AI services, and mobile network operators.

What Is Changing

The strongest recurring theme is the paradigm shift from connectivity as a terrestrial infrastructure problem towards integration of space-based computing and networking nodes. Traditionally, satellite internet served as a last-mile or resilient backup option, often falling short of enterprise-grade speed and latency needs (Vortex IT Systems 2026). However, the planned deployment of AI-processing orbital data centers aboard SpaceX’s Starship deployments signals an architectural transformation. This could unlock low-latency, globally consistent AI services impervious to terrestrial infrastructure outages (CNN 24/06/2026).

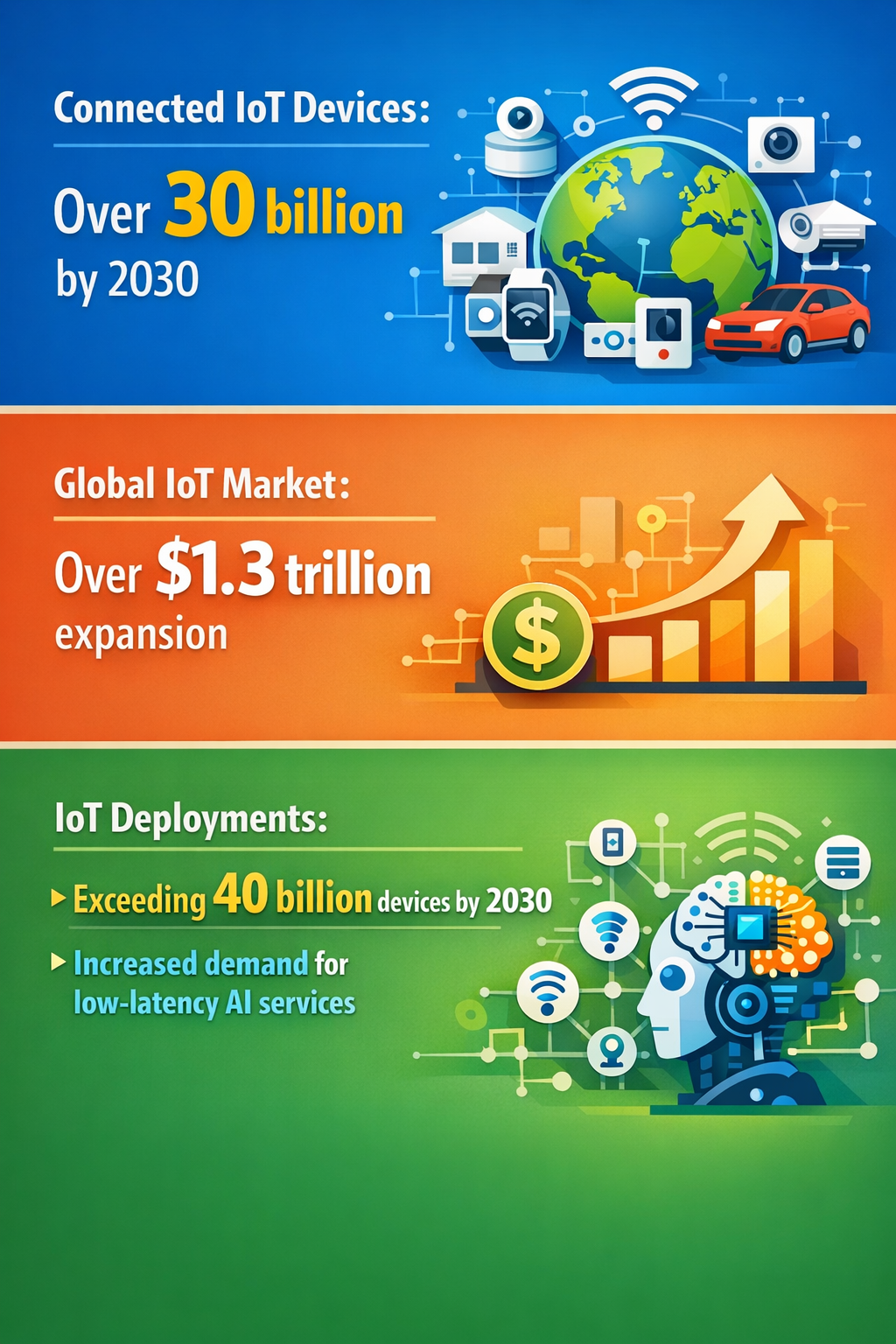

Simultaneously, the anticipated explosion of IoT devices (expected to exceed 40 billion by 2030) is dramatically increasing demand for low-latency AI services at the edge (Persistence Market Research 2026). Terrestrial 5G and upcoming 6G networks alone may struggle to meet these requirements due to physical and regulatory constraints. Space-based edge computing directly responds to this gap, enabling AI and data processing to occur closer to devices worldwide regardless of location or local infrastructure quality (IEEE Spectrum 2026).

Furthermore, 6G radio infrastructure investment projections (from $8.1 billion in 2029 to $67 billion by 2034) overlook the disruptive potential orbitally deployed resources represent, as they could lessen demand on terrestrial infrastructure while increasing competitive pressure on traditional mobile network operators (ABI Research 2026). For instance, SpaceX’s announced intention to target the US mobile consumer market with Starlink mobile service threatens to alter incumbent operators’ market structures (Fierce Network 2026).

Crucially, this move introduces a new cybersecurity dimension, as space-based network and ground stations become critical infrastructure requiring sophisticated US space cybersecurity solutions (Polaris Market Research 2026). This is an often-overlooked systemic shift, indicating an expanded attack surface and new regulatory requirements for protecting orbital assets.

Disruption Pathway

The pathway towards structural change begins with technical and commercial deployment of AI-processing satellites coupled with low earth orbit constellations achieving robust, low-latency connectivity.

Accelerating conditions include rapid growth of IoT and AI-as-a-service demand, coupled with terrestrial network spectrum scarcity and infrastructure rollout delays that constrain 5G/6G network performance (Persistence Market Research 2026). This supply-demand mismatch will incentivize capital shifts toward orbital edge networks that better deliver global ubiquitous AI services.

As orbital nodes increase in number and capability, legacy telecommunications operators face pressures to partner, compete with, or potentially be displaced by satellite-based operators. This introduces stress in industrial structures, especially in spectrum allocation, roaming agreements, and cross-jurisdictional governance frameworks (Fierce Network 2026).

Regulatory adaptations will be needed to address spectrum sharing, orbital traffic coordination, data sovereignty in space, and cybersecurity mandates to protect AI-processing satellite clusters and ground infrastructure (Polaris Market Research 2026). Early regulatory fragmentation could create interoperability challenges but also incentivize standard-setting coalitions.

Feedback loops may emerge as more AI services migrate to space, enhancing satellite autonomy and data processing efficiency, which in turn fuels further AI adoption. Unintended consequences might include increased orbital debris hazards and geopolitical tensions over orbital resource control.

Under these conditions, traditional telecom and cloud service delivery models might shift towards hybrid mesh paradigms where orbital compute nodes act as critical infrastructure nodes—forcing a reevaluation of industrial strategies, capital allocation, and legal frameworks across government and industry.

Why This Matters

From a capital deployment perspective, investors may need to reconsider portfolio exposures to terrestrial-only 5G/6G infrastructure in favor of satellite-based AI-edge compute platforms. Telecom operators must address competitive threats from vertically integrated space services providers.

Regulators face a novel challenge: extending spectrum governance and cybersecurity measures into space, including novel forms of data sovereignty, liability for space-based AI processing, and cross-border coordination to mitigate emerging geopolitical risks.

Supply chains could be reshaped as satellite manufacturing, launch services, and space-based semiconductor fabrication systems accelerate, creating new industrial clusters with different risk profiles compared to terrestrial network equipment.

Liability regimes could shift to include space-based data processing errors and AI decision failures, prompting insurers, policymakers, and operators to develop new frameworks.

Implications

This orbital edge computing development may fundamentally alter the connectivity ecosystem by decentralizing data processing and introducing new trust and governance layers extended into space.

It is likely to enable novel AI service models that are impossible or economically infeasible on earth-bound platforms, reshaping end-user experiences globally, especially in underserved regions.

This structural change should be distinguished from transient hype cycles about 6G or incremental satellite internet improvements; it represents a systemic architectural evolution merging multiple technology trajectories (AI, IoT, satellite constellations).

However, skepticism persists that orbital AI centers might not scale efficiently due to power, thermal, or latency constraints—though ongoing R&D efforts and planned deployments challenge this view.

Some may interpret this as simply a new layer of satellite internet, missing the far-reaching impact orbital compute nodes could exert on digital infrastructure and governance.

Early Indicators to Monitor

- First commercial launches and operationalization of AI-processing orbital data centers (e.g., SpaceX Starlink next-gen satellites) (CNN 24/06/2026)

- Patent filings and R&D disclosures related to satellite-based AI edge computing hardware and software

- Venture capital clustering on startups integrating AI with satellite communication platforms

- Draft regulatory proposals addressing space-based spectrum sharing, AI data processing, and cybersecurity rules (Polaris Market Research 2026)

- Capital reallocation trends shifting budgets from terrestrial 6G rollout towards satellite infrastructure and hybrid connectivity solutions (ABI Research 2026)

Disconfirming Signals

- Failure to launch or operationalize orbital AI-processing nodes at scale within the next 5 years

- Advances in terrestrial 6G and AI edge infrastructure that fully address low-latency global coverage without space integration (The Register 27/05/2026)

- Significant orbital debris incidents leading to major network outages or new restrictive regulation

- International regulatory impasse or geopolitical conflicts freezing cooperative frameworks for space-based spectrum and AI data governance

- Economic or technological failures in maintaining power, thermal management, or maintainability of orbital AI compute centers

Strategic Questions

- How should capital allocation shift to hedge or capture growth opportunities in hybrid terrestrial-orbital connectivity architectures?

- What regulatory and governance models best balance innovation, security, and sovereignty over space-based AI-processing infrastructure?

Keywords

Orbital Edge Computing; 6G; AI in Orbit; Starlink; Satellite Internet; Space Cybersecurity; Connectivity Infrastructure; Internet of Things

Bibliography

- Starship is slated to carry the next generation of Starlink internet satellites to orbit and deploy SpaceX's envisioned AI-processing orbital data centers. CNN. Published 24/06/2026.

- SpaceX told investors that it plans to launch a new Starlink mobile service for U.S. mobile consumers that would put it in direct competition with AT&T, T-Mobile and Verizon. Fierce Network. Published 2026.

- IoT deployments are expected to exceed 40 billion connected devices globally by 2030, significantly increasing demand for low-latency AI services. Persistence Market Research. Published 2026.

- US space cybersecurity solutions are designed to safeguard satellite internet, satellite ground stations, and space-based communication systems from digital threats. Polaris Market Research. Published 2026.

- 6G radio revenue will increase from US$8.1 billion in 2029 to roughly US$67 billion by 2034. ABI Research. Published 2026.